The Covid-19 pandemic has changed what we do and how we do it. Consumer habits typically evolve over time, but Covid-19 has abruptly changed how we live, shop and consume. The question is, which behaviours will linger and which will be dropped?

Covid-19 magnified the relevance of many categories and products and significant changes in shopping behaviours occurred in supermarkets. In February, when NZ identified its first Covid-19 case, Kiwis flooded supermarkets to panic buy, causing widespread out-of-stock issues. In the week ending 1 st March, Prepackaged Grocery rose +14.4% over the same week last year. On March 26 th level 4 lockdown was implemented and value growth shot up further, +29.5% (week to 29 th March). Overall, level 4 (5 weeks to 26 th April) achieved impressive growth of +25.0% compared with a year ago.

Today, in level 1 (7 weeks to 26 th July), as ‘normality’ returns, growth remains high at +6.4% [3] , but a number of ‘essential’ categories have contracted versus the highs of level 4.

However, overall Prepackaged Grocery is showing no signs of slowing down, with sales up +7.1% in the week to 26 th July.

What was on the menu?

Shoppers flocked the Baking & Cooking, Frozen and Dairy departments during level 4, experiencing significant combined growth of +37.7% in dollar sales and accounting for 33.1% of store vale sales, up +3.1 share points on last year [2] . Growth of these departments softened in level 1 to +8.2%, however still ahead of 2019 [3].

During level 4 as we cooked more, categories such as Milk & Cream (+20.7%), Eggs (+34.4%), Dairy Spreads & Fats (+43.0%) and Cheese (+32.3%) all experienced strong sales performance [2] . Baking became the ‘iso thing to do’ during lockdown and the Baking & Cooking department saw significant growth of +52.5% on last year. Cake Needs (+99.6%), Flour & Mixes (+120.4%) and Sugar & Sugar Substitutes (+51.8%) all experienced solid growth [2] .

Since levelling down, growth rates across all of these categories has softened notably as Restaurants and Cafes re-opened.

In-Home dining

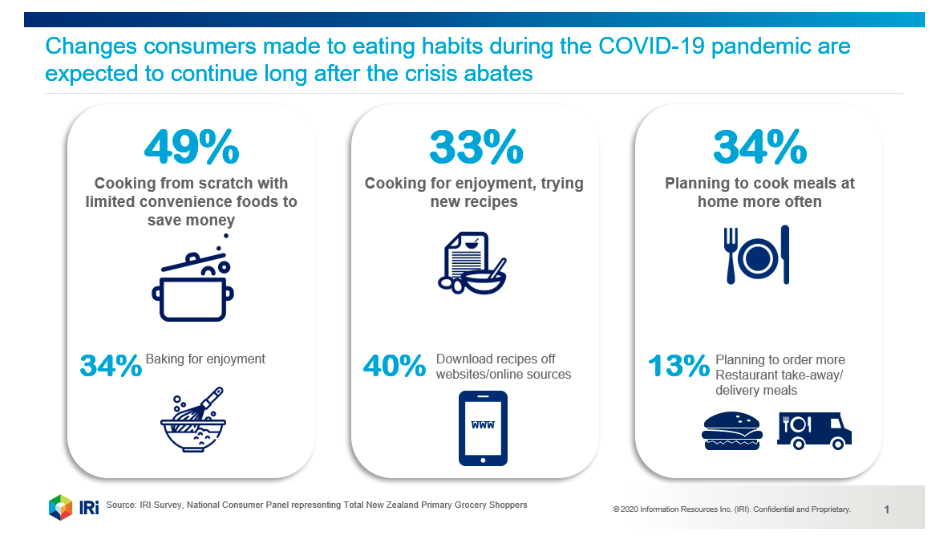

Kiwis missed their restaurant and café ‘fix’ during lockdown. In a typical week, 40% of us would eat in a restaurant or café while 60% would purchase take-out or home delivery [1].

Prior to Covid-19 consumers were time poor, averaging 32 minutes cooking main meals on weekdays and always looking for ‘shortcuts’ [1]. During level 4, as we were forced to stay home, time was plentiful, with more home cooking from scratch. Accordingly, categories such as Dried Pasta (+37.9%), Rice (+19.4%), Oils (+44.7%) and Shelf Stable Pasta Sauces (+42.5%) all saw impressive growth on last year [2].

Consumers experimented, trying to bring the restaurant experience home. Recipe enhancers such as Herbs & Spices (+73.9%), Stock (+52.8%), Seasoning & Crumbs (+38.4%) all grew significantly compared to a year ago [2]. Again, we see growth ease for most of these categories in level 1 but still remaining above 2019 levels as patronage at Restaurants and Cafés has yet to return to pre-covid levels.

‘Appetite for Experimentation’

Travel restrictions mean we’re craving ‘new experiences’, making food choices more ‘International.’ Even in normal times 55% of Kiwis “like to be inspired to try new things” and over half “like to try exotic and interesting flavour choices” [1]. Unsurprisingly during level 4, ethnic categories like Mexican, Asian and Indian were up +48.9%, +63.1% and +56.2% respectively, as more of us attempted to make a Burrito, Pad Thai or Butter Chicken. Growth of these categories has relaxed but continues to be elevated in level 1 compared to 2019.

Efforts to add authenticity have seen related segments grow rapidly, including Asian and Indian Bottled Sauces, Pastes and Simmer Sauces. Dining aspirations have also boosted ‘appetisers’ and the Frozen aisle, with considerable growth in Asian Snacks up +78.4% during level 4[2] and +19.7% in level 1[3] compared to the same period last year.

I’m over it, help!

The monotony of lockdown and cooking from scratch took its toll. Some clearly wanted the ‘total package’ from the supermarket, which boosted products during level 4 such as Frozen Pizzas (+98.8%), Frozen Meals (+15.9%) and Frozen Pies (+76.2%) [2].

Frozen Value-Added Chicken also grew strongly over this period (+108.0%), with brands like “Tegel Take Outs” mimicking takeaway favourites up +354.0% on last year [2] and continuing to deliver triple digit growth in level 1 +277.1% [3]. Beyond meals, ‘help-me’ solutions such as Baking Mixes and Cake Mixes reported triple-digit growth, +105.1% and +136.3% respectively [2].

Convenience gets competitive

Meal Delivery Kit services have been tried by 9% of Kiwis at some point, and 5% used them in the last month [5]. A Canstar Survey reported 52% of respondents chose them for their convenience and 47% felt they’d tried a more diverse range of food as a result [4]. Within supermarkets, International Meal Kits delivered +$1.8 million (+49.2%) value growth during level 4 [2] and continues to perform well in level 1 +11.9% [3].

So, in summary, there have been many big consumer behavior changes under lockdown level 4 and whilst many categories continue to see elevated growth in level 1, the next few months will start to show us if this will be the new normal.

Sources:

[1] IRI NZ 2018 State of the Industry Survey

[2] IRI MarketEdge (Grocery) New Zealand Value [5 weeks to w/e 26/04/20]

[3] IRI MarketEdge (Grocery) New Zealand Value [7 weeks to w/e 26/07/20]

[4] https://www.canstarblue.co.nz/food-drink/meal-kit-delivery/

[5] IRI NZ 2019 State of the Industry Survey

Author: Pravina Patel, Market Insights Lead at IRI.